Out of the Fire: Repositioning Independent Distribution

Part Two: After the Fire

by Neil Gillespie and Allen Ray

Part One of our series looked at how the fire was started: by economic intervention that created “bubble” demand and extremely liberal credit. The result was an economy with poor roots. The growth distributors enjoyed was unsustainable, so planning baselines have shrunk to minus 20% or worse. Distributors reacted defensively to protect current business, while cutting back on people and expenses. Better performers, however, looked deeper for answers in more places. Some even touched on the key to genuine growth opportunities, which we will point out in this edition.

Part One of our series looked at how the fire was started: by economic intervention that created “bubble” demand and extremely liberal credit. The result was an economy with poor roots. The growth distributors enjoyed was unsustainable, so planning baselines have shrunk to minus 20% or worse. Distributors reacted defensively to protect current business, while cutting back on people and expenses. Better performers, however, looked deeper for answers in more places. Some even touched on the key to genuine growth opportunities, which we will point out in this edition.

Here’s a complete list of the findings once more. We’ll pick up at finding six in this article.

1) Past growth was largely artificial: the new planning baseline is -20% or worse

2) Distributor reactions were primarily defensive

3) GP%, inventory turns, receivables performance slipped a bit, net profit a lot

4) Good performers tend to be realists vs unbridled optimists

5) Good performers looked deeper for answers and in more places

6) Surprise: good performers cut more sales people (What do they know?)

7) Everyone is afraid of “the weather” (the direction of the nation)

8) Growth opportunities: the usual sources won’t deliver, the new sources are still “suspect”

9) Distributors need to broaden their growth horizons while improving productivity to increasingly turn gross margin dollars into profits

10) Manufacturers executed their usual tactics to curtail expenses

Diving InTo Each

6) Surprise: Good performers cut more salespeople

As a reminder, good performers are defined as those with sales variances of -5% or better. Poor performers had 20% or greater declines. There were fewer good performers, as you might expect.

Here’s the really interesting points:

- Good performers had almost twice the tendency to cut inside sales

- Good performers had almost 70% higher tendency to cut outside sales

- Good performers had roughly half the tendency to cut travel and entertainment (T&E) expense

We suspect that good performers understand the concept of marginal profits when volume rises. You keep people when they are marginally profitable. Like we said, if there hasn’t been a fire in a while, these people can produce some profit, but not as much as the really good people. In a fire, they turn unprofitable. You probably should have let them go if you could have found a better salesperson before the recession. Since they are not that good, it’s logical to cut them.

You may still be scratching your head about the T&E expense. So did we, at first. Good performers cut this a little, but didn’t cut off the resources to their better performing salespeople. They needed to keep customers in the game. T&E helps you stay close to customers: the number one baseline action in a recession. So does marketing expense. Good performers cut this less as well.

Conclusion: Good performers let the fire do its work with marginal performers. They keep funding things that help good sales producers stay close to the customer.

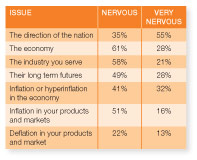

7) Everyone is afraid of “the weather”

We suspected that many businesses were reluctant to invest due to the extremely “different” direction of the federal government. The health care bill, cap-and-trade, TARP bailouts, takeover of General Motors, heavy-handed investments of taxpayer money in major banks, plans for increased marginal tax rates, hidden future payroll tax increases and frozen credit has independent business owners in a funk on business investment, hiring and general optimism.

Independent business people tend to be politically conservative. Many are Subchapter S Corporations or Limited Liability Corporations with pass-through income that will be severely threatened if the current administration gets its way with taxes. Small businesses with 500 employees or less create over 60% of new jobs in this country but the government seems to be ignoring that despite executive branch lip service.

Independent business people tend to be politically conservative. Many are Subchapter S Corporations or Limited Liability Corporations with pass-through income that will be severely threatened if the current administration gets its way with taxes. Small businesses with 500 employees or less create over 60% of new jobs in this country but the government seems to be ignoring that despite executive branch lip service.

Our survey respondents are nervous about all this. When it comes to the direction of the nation, they are very nervous.

This is affecting how they think about the economy, their industry and their long-term futures. We suspect that when the offending legislation has all passed (or not) and we know what we’re dealing with, some of the uncertainty will lift and business will get a little better. Maybe.

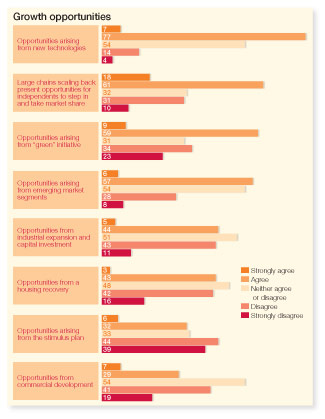

8) Opportunities: The usual suspects won’t deliver growth, the new suspects are purely “suspect”

Distributors don’t think residential, commercial or industrial expansion will deliver the growth as in the past. Whereas they are probably correct, their thoughts on the sources of growth sound like they swallowed the green Kool-Aid. When asked to indicate where growth will materialize, energy, wind power, solar power and LED lighting dominate the answers. They tend to think of these as both technologies and market segments, as they show up as open-end answers to questions about growth prospects in both these areas.

We can forgive them. They don’t have much to go on besides the green stuff.

We can forgive them. They don’t have much to go on besides the green stuff.

During 2003-2008, housing led the way for the rest of the economy but that bubble violently exploded. Will solar, wind and LED lighting be nearly as big? Most likely they will be nice niches, but neither artificial bubbles nor major sources of sustainable growth unless you’re a niche player. Time to look for more ways to grow.

Independence can be an advantage

The feistier independent businesses (about 20% of the respondents came from national chains) indicated they had an opportunity to gain share vs.

national chains that cut back resources in their markets. They could be right. We interviewed some distributors whose owners stepped up their personal calls on key accounts. An owner with decision-making autonomy beats a branch manager without, goes their theory. You can be your own judge of that, but we tend to think it’s true. The best independent distributor in a trading area is almost always the market share leader in a segment like industrial, OEM, project construction or residential construction. Why not get out there and test your strength some more? Go with what you are.

9) Distributors need to broaden their horizons for future growth

Taking more risk leads to higher returns. Serving the same markets in a flat to shrinking market yields steady decline.

So what are distributors waiting for? The survey responses overwhelmingly indicate that distributors rush to protect key accounts. But they get less and less aggressive when it comes to getting more from current accounts, taking share from competitors’ customers, launching new product lines, approaching new market segments, expanding geographically or tackling even more exotic growth strategies like vertical integration.

So what are distributors waiting for? The survey responses overwhelmingly indicate that distributors rush to protect key accounts. But they get less and less aggressive when it comes to getting more from current accounts, taking share from competitors’ customers, launching new product lines, approaching new market segments, expanding geographically or tackling even more exotic growth strategies like vertical integration.

When asked what they would have done differently or done more of, most distributors offered ideas in this general order:

1. Better asset management, especially inventory: cut sooner to conserve cash

2. Cut headcount expenses sooner

3. Step up sales aggressiveness

4. More expansive marketing strategies before the recession started

The bigger thinkers thought it was a good idea to expand geographically with startups and acquisitions before the recession. They mentioned getting into different market segments and selling different products they didn’t sell yesterday. They think of growth as additional sources of profits that will help them weather the storm. We’ll bet they think like Chuck Steiner of Branch Electric did years ago. “Don’t put in a 10-person branch when a two-person branch will do.” There is a way to do it without betting the whole farm. Get his CD from NAW and listen well. Steiner overstocked “A” items to increase his service advantage in the last recession he faced.

He profited handsomely especially when the market started growing again.

This open-end comment holds the most promise, though:

“We changed our market focus and adapted our company to focus on niche markets. It has worked very well. Our sales are flat to slightly increased while our competition is off 30% or more.”

We love this person, wherever he or she is. The respondent didn’t leave identification on the survey, but did leave a big clue for the rest of us. The more you specialize in something, the better you become, so segment your business into niches and create differentiated offerings to each. This company seems to have touched on the first fundamental of growth: optimize your core, and then add more segments to it. We hope that person is reading this, because he or she will probably get right on the things we say next, if not already.

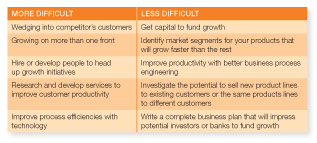

Distributors struggle to grow on multiple “fronts” and with optimizing operations productivity. The answers to what they struggle with must be interpreted, however.

Since we think distributors have a more narrow definition of growth opportunities than we think is healthy, their definition of “fronts” is narrower than ours. If they broadened it, “Growing on more than one front” might rise to the top of the difficulty list. If they realized that a business plan included plans for distinct market niches with descriptions of value propositions, operations, sales, products, services, marketing and individual pro-forma contributions, they might not be so quick to say it was easy.

If business plans are so easy and it’s easy to get capital for growth, then why did a third of credit applicants get turned down and two thirds of them get less than half of what they asked for? Sounds like the business plan isn’t fetching many admirers. Banks rent money. They want you to show them where the money will come from and how you’re going to get it. Not to mention some liquid collateral.

That dead inventory and glob of receivables over 90 days doesn’t qualify. When you’re shrinking, you tend to accumulate more of these. That’s why you get a lower line of credit against your current assets.

Conclusion: Develop a new framework for thinking about an expanded set of growth opportunities. Do this on a platform of increased core productivity. This will grow the rate of profit as well, generating dramatically more cash and retained earnings, not just revenue.

10) Manufacturer actions: The usual

Distributors spotted manufacturers doing the same things they usually do in recession, only more. They cut back technical support, field sales and co-op marketing expense. They stepped up share-gaining tactics like inventory buyouts to get on shelves a little bit. They tightened up a little bit in a number of areas like SPA claims and returns, but not much. Most of what they squeezed, according to our respondents, was field and technical support headcount and funding co-op marketing. These things have the biggest short- to medium-term payoff.

Part II: REBUILDING WITH A STRONGER CORE

Analyzing how organizations react under pressure delivers starter clues for how to grow. For example, most distributors rush to protect and grow existing customers. Some graduate to taking share from competitors. Those are the first things you do. But what else?

If you reverse the movie on decline, you can see how things grow. Here’s how: Just like listening and responding to customers can create whole new businesses and brings in more revenue, reversing the process and limiting your activity to pursuing orders for existing products without listening for new opportunities is slow destruction. You’re turning the wheel the wrong way, you’re not looking out on the edges of your business for growth.

Neil Gillespie is a veteran distribution consultant, speaker and author. Neil worked for GE and Eaton corporations before launching his distributor consulting practice in 1995. He helped Roden Electrical Supply of Knoxville grow more than 500% over 11 years, while more than tripling EBITDA percentage. Neil has distilled his profitable growth methods in his Eight Steps to Breakthrough Growth. His book “Discover Your Core, Then Go For More” is now available. Contact Neil at neilg@shamrockgrowth.com.

Neil Gillespie is a veteran distribution consultant, speaker and author. Neil worked for GE and Eaton corporations before launching his distributor consulting practice in 1995. He helped Roden Electrical Supply of Knoxville grow more than 500% over 11 years, while more than tripling EBITDA percentage. Neil has distilled his profitable growth methods in his Eight Steps to Breakthrough Growth. His book “Discover Your Core, Then Go For More” is now available. Contact Neil at neilg@shamrockgrowth.com.

Allen Ray has 45 years of experience as a distribution business owner, information systems, marketer of product data and consultant to wholesale distributors. Allen advises clients on strategies to stop “Profit Leakage” and create a scalable business that returns an increasing percentage of gross margin dollars to net profits. Allen is collaborating with Neil to help distributors adopt the Eight Steps to Breakthrough Growth, providing expertise in “Leadership Productivity” and “Pricing for Maximum Gross Profit Dollars per Order.” Contact Allen at allen@allenray.com.

Allen Ray has 45 years of experience as a distribution business owner, information systems, marketer of product data and consultant to wholesale distributors. Allen advises clients on strategies to stop “Profit Leakage” and create a scalable business that returns an increasing percentage of gross margin dollars to net profits. Allen is collaborating with Neil to help distributors adopt the Eight Steps to Breakthrough Growth, providing expertise in “Leadership Productivity” and “Pricing for Maximum Gross Profit Dollars per Order.” Contact Allen at allen@allenray.com.

This article originally appeared in the March/April 2010 edition of Industrial Supply magazine. Copyright 2010, Direct Business Media, LLC.

INDUSTRIAL SUPPLY MAGAZINE

The July/August issue of Industrial Supply magazine features an in-depth cover story about Global Industrial. Plus, we're featuring articles by contributing writers Dr. Bharani Nagarathnam and Frank Hurtte, as well as interviews with numerous product and distribution industry experts.